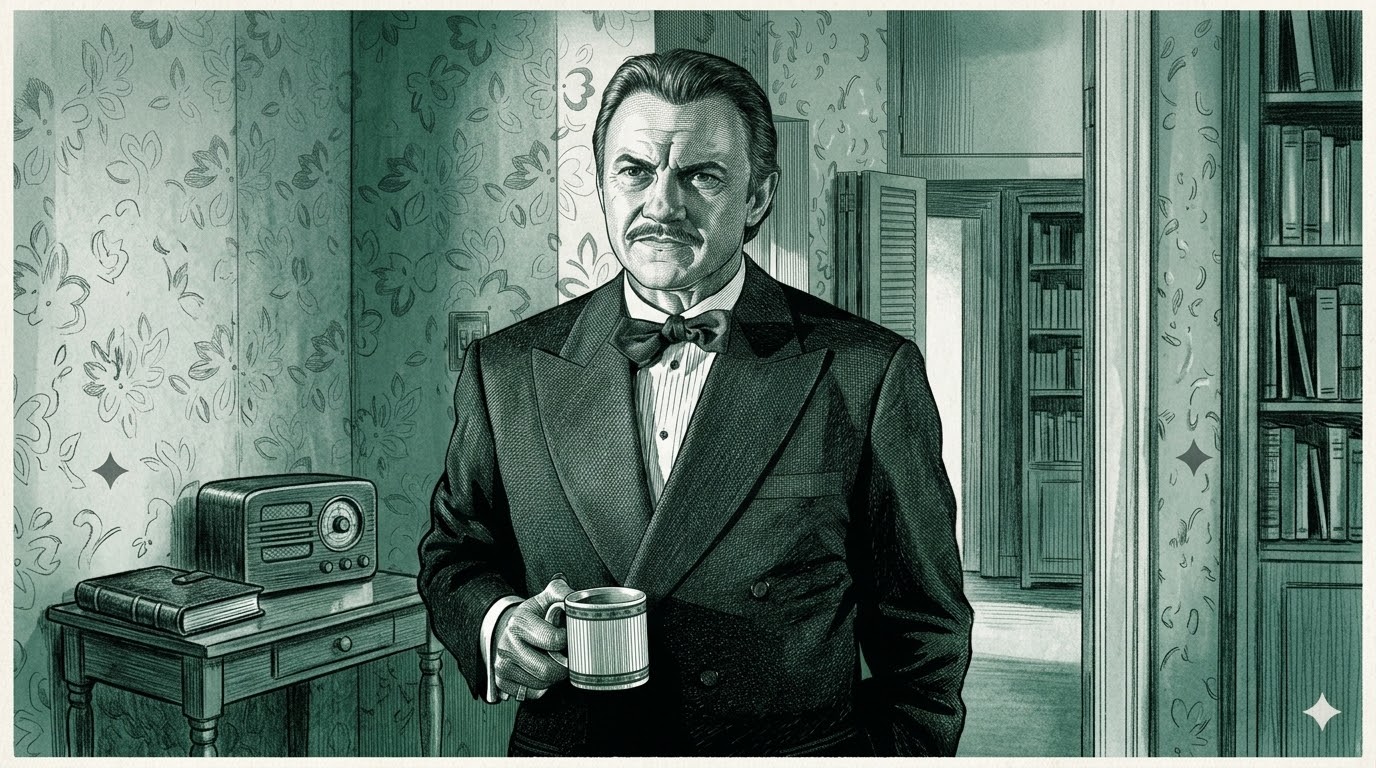

The Wolf

The AI labs just spent $10 billion hiring ten thousand of him, because the one thing they can't rent is a way into your building.

THE NUMBER: 42x — the growth in forward-deployed engineer job postings from 2023 to 2025, per LinkedIn data, against 13x for traditional AI engineering. The fastest-growing job title in artificial intelligence is a human being who installs it. Five companies backed that title with roughly $10 billion of committed capital in twelve months, because intelligence stopped being the bottleneck and deployment became it. Hold that number. The whole issue hangs off it.

On Monday, Tomasz Tunguz did the thing he does better than almost anyone in the venture business: he added up a bill nobody else had bothered to total. AI companies have committed roughly $9.75 billion in twelve months to forward-deployed engineering — human engineers, embedded inside customer organizations, whose job is to make AI actually work. Not train it. Not benchmark it. Install it.

The line items read like a capital markets story, because they are one. OpenAI raised $4 billion of external capital for a standalone Deployment Company at a $14 billion post-money valuation, TPG-led, nineteen investors deep. Anthropic pulled $1.5 billion into a joint venture from Blackstone, Hellman & Friedman, Goldman Sachs, Apollo, and General Atlantic. Amazon committed $1 billion off its own balance sheet. Google Cloud put $750 million into a partner fund. And Microsoft stood up its Frontier Company internally — a 6,000-person deployment division run by its former Asia president — the same week it cut 4,800 jobs from Xbox. OpenAI even bought a whole firm to get moving faster: Tomoro, a 150-person Edinburgh consultancy whose client list runs from Tesco to Fidelity to the NBA. Salesforce has committed to 1,000 forward-deployed roles of its own.

Sit with the shape of that for a second. The industry whose entire pitch is the replacement of human labor is in a bidding war for human labor. Nobody involved thinks that’s a contradiction, and they’re right — it isn’t. It’s a confession. The models are good enough. The organizations aren’t. And the gap between those two sentences is now a ten-billion-dollar asset class.

🎬 I’m Winston Wolf. I Solve Problems.

You know this character, even if you’ve never heard the term FDE.

It’s 8:30 in the morning in Pulp Fiction. Jules and Vincent have a body in the car and a kitchen that looks like a crime scene, because it is one. And into Jimmie’s house walks a man in a tuxedo — from some party he never bothers to explain — who introduces himself with the cleanest job description in the history of American cinema: “I’m Winston Wolf. I solve problems.”

Watch what the Wolf actually does, because it’s a management clinic. He doesn’t touch the body. He asks precise questions, inventories the resources on hand (cleaning products, blankets, a bathroom), assigns the work to the people already standing there, sets a deadline driven by an external constraint, and inspects the output. Forty minutes, gone in the Acura. The mess was never his mess. His product was the procedure.

That is a forward-deployed engineer. The FDE shows up inside your company, takes over the kitchen, wires the frontier model into your claims workflow or your underwriting desk, teaches your people to run it, and leaves. Palantir invented the role two decades ago; the name itself is borrowed from the military, and the military etymology is the part everyone quotes and nobody thinks about. Forward-deployed forces are not a permanent posture. Advisors embed, train the locals, and hand over the keys. The end state of forward deployment is withdrawal. That’s true of special forces, it’s true of the Wolf, and it’s about to be true of the highest-paid job title in software.

Nobody keeps the Wolf on payroll. Remember that; the whole back half of this issue depends on it.

💼 Who’s Buying, Who’s Renting

Now put last week’s loudest television appearance next to Monday’s quietest capital table, because together they draw the actual battle map.

Alex Karp went on CNBC ostensibly to announce a partnership, and instead delivered the rant everyone clipped: enterprises are getting “no value” from tokens, the labs are after your IP, and — the line we ran on July 1 — “if it was so valuable, wouldn’t I say I’ll make you $1 billion and I want 30 percent?” Fortune spent this week fact-checking the rant and caught the self-serving part: outcome pricing isn’t Karp’s thought experiment, it’s literally Palantir’s rate card. Everyone in this story is talking their book. That’s fine. Books are information.

Because look at what Karp was actually there to announce: Palantir plus Nvidia, “sovereign AI infrastructure” for the U.S. government and critical industries — Nvidia’s open-source Nemotron models running underneath Palantir’s application and governance layer. Read that trade twice. The man who owns the distribution just sourced his intelligence from the free bin. Karp is betting the model is a commodity component, and he’s structurally positioned so that the better the open floor gets, the fatter his margin gets.

The labs are running the mirror-image trade, and it’s costing them ten billion dollars. They own the intelligence and cannot buy their way into the customer’s building fast enough. That’s what the PE structure of these deployment ventures is really about: Blackstone alone holds 275 portfolio companies, and Anthropic’s JV targets them first. The private equity firms aren’t providing capital — the labs have capital. They’re providing introductions. Pre-sold trust, at scale, to companies they already control.

And the fine print tells you who thinks they’re holding the risk. OpenAI’s Deployment Company guarantees its PE backers a 17.5% return floor. When your partner negotiates a guaranteed floor on your shared upside, they’ve told you their honest estimate of the execution risk — and it isn’t low. The FDE org serves two masters: the lab wants maximum deployment, the PE wants its floor, and when those goals collide, guess which one has it in writing.

Here’s the asymmetry underneath all of it, and it’s the sentence to carry out of this section: Palantir can rent a model. The labs cannot rent distribution. Everything else — the JVs, the Tomoro acquisition, the 6,000-person internal army, the 17.5% floor — is the price of that one sentence.

It also means you need to rethink the M&A board. The rumor that OpenAI might try to acquire a major SaaS player—say, Salesforce or ServiceNow—makes mathematical sense when you view it through this lens. If the only way to monetize a $100-billion intelligence factory is to own the last mile to the customer, you don’t build the last mile from scratch. You buy it. But integrating a legacy software stack with a frontier model is the hardest M&A integration problem imaginable, and OpenAI’s DNA is research, not enterprise integration.

Which is why the alternative is more likely: the labs don’t buy the software layer, they buy the services layer. The integrators. The consultancies. If you’re OpenAI, do you buy Salesforce and try to rebuild it, or do you buy a major systems integrator—an Accenture or a Slalom—and just embed your model into every transformation project they run? If the name of the game is Git-R-Done, you buy the people who already know how to get it done inside the enterprise.

But the currency is the easy half. The hard question, the one that actually matters: what did one of the most valuable companies on earth decide was worth sixty billion?

Not a model. That’s the thing people keep missing. Cursor is the biggest coding shop on the planet that isn’t a frontier lab — roughly $2.6 billion in annualized revenue, mostly enterprise, growing fast. What makes it worth sixty billion isn’t a clever model. It’s that Cursor sees more cutting-edge code, written by more real developers solving more real problems, than anyone alive. He didn’t buy a tool. He bought a sensor — the single best-positioned sensor in existence for watching how software actually gets made.

The rest of the field is arriving at the same place from every direction at once. Ben Evans’s Sunday column was titled, simply, “AI Deployment companies” — his framing: giving everyone Copilot mostly failed, point solutions are struggling, and the next phase is bespoke integration. Ethan Mollick echoed the same sentiment on X this morning, noting that “we have AI” is no longer a differentiator; “we have an AI that actually changed our workflow” is.

What this means for your team: the hiring spec you wrote in 2023 is backwards. Stop screening for the skill the model just commoditized and start screening for the judgment it has to be trained on. And today, not this quarter: hand your best non-technical domain expert an agent and one real task. The five-point gap says they’ll be fine. The bottleneck was never the syntax.

📉 We Have a Website

We’ve seen this movie, and the last time it played the year was 1999.

Back then the magic words were “we have a website.” Every company put up a page, slapped a dot-com on the logo, and told investors the future was handled. For about eighteen months the market paid for the pitch: it valued eyeballs and page views, the presence of the thing rather than the profit from it. Then, on a schedule nobody controlled, it stopped grading the pitch and started pricing the P&L. Having a website turned out to be table stakes, and the companies that could only say they had one, instead of showing what it earned, got repriced toward zero. The web was completely real. “We have a website” was still worthless.

“We have AI” is the 2026 version, word for word. A company can still get a nod in a board meeting for it today. That window is closing exactly the way the last one did, and Tunguz’s minus-36 is the sound of it closing. The technology is real, realer than the web was and moving ten times faster. But the claim is deflating to nothing, because the claim was always talk, and talk just went free.

The bottom line: Presence was the last era’s currency. Output is this one’s. If your AI story is a pilot and a press release, you’re holding 1999’s website.

What This Means For You

The stories rhyme because they’re the same story: talk got free, so the market repriced everything around what actually gets finished. Three moves, whichever chair you’re in.

Sort your software budget into “token path” and “seat.” Tunguz drew the map — infrastructure and security compound, per-user seats get substituted and are already down 36%. Label every line on your renewal list this week and walk into the seat renegotiations before the vendor reprices for you.

Route the bulk work to the worker tier, and measure what it finished, not what it burned. Sonnet 5 at two-and-ten is built for the agentic jobs running up your bill; save frontier tokens for the work that earns them. And kill the usage leaderboard — Meta ranked people by tokens consumed and Amazon shut its version down with a memo reading “don’t use AI just for the sake of using AI.” Consumption isn’t accomplishment.

Dual-source before the gate swings back. Eighteen days dark, then restored just as fast, at the discretion of people who don’t answer to you. Stand up an open-weight model you control for anything you can’t afford to have gated on someone’s bad afternoon.

Git-R-Done stopped being a punchline this week and became the business model. Show what got finished, or get repriced for talking about it.

Three Questions We Think You Should Be Asking Yourself

- If the market ran the Git-R-Done test on my company, would I pass? Not “do we use AI” — every deck says that. Can you name work that got finished, a cost that came down, a cycle that got shorter, and attribute it? If the honest answer is a pilot and a press release, you’re on the wrong side of the minus-36.

- Which of my software line items is a seat, and which is a token path? One bucket is compounding and one is being substituted. If you can’t sort your own stack, your vendors already have, and they’ll price accordingly.

- When the gate closes again, what am I running on? It will close again — the last eighteen days were a preview, not an accident. If your whole operation depends on a frontier model the government can switch off, you don’t have a strategy. You have a single point of failure with a marketing budget.

— Harry and Anthony

Sources

- The $10B FDE Boom — Tomasz Tunguz, Jul 7, 2026 (the $9.75B capital table; 42x vs 13x LinkedIn data; the three structural models; the 17.5% return floor; Tomoro acquisition; Blackstone’s 275 portfolio companies; Salesforce’s 1,000 FDE roles)

- Benedict’s Newsletter No. 650 — “AI Deployment companies,” Jul 5, 2026 (Copilot’s failure, “automation requires a lot of manual labour,” Microsoft/Amazon/WPP announcements, McKinsey’s “>30% of fees” on outcomes; ben-evans.com)

- Palantir CEO Alex Karp is wrong about the threat Anthropic and OpenAI pose to most enterprises — Fortune, Jul 7, 2026 (the CNBC rant, the Palantir–Nvidia Nemotron partnership, the outcome-pricing catch)

- Satya Nadella announcing Frontier Co. — X, Jul 2, 2026 (“a learning loop in which human capital and token capital compound”)

- Microsoft reportedly ditching OpenAI’s and Anthropic’s models to cut costs — SiliconANGLE, Jul 7, 2026 (Bloomberg report; MAI routing)

- Why Anthropic bet on adult supervision for tokens — The Deep View, Jul 7, 2026 (Claude Enterprise spend alerts, cost-vs-output analytics, model defaults by role; Ramp: 77% of frontier-LLM orgs on Anthropic)

- Anthropic, “A global workspace in language models” — transformer-circuits.pub, Jul 6, 2026 (the 25-slot workspace; the 59%-vs-5% swap experiment)

- Ramp Economics Lab × Revelio Labs, “Companies hire more after AI adoption” — Jun 30, 2026 (21,000 companies; +10% headcount, +12% entry-level)

- Microsoft cuts 4,800 roles — Reuters, Jul 6, 2026

- Alfred D. Chandler Jr., The Visible Hand: The Managerial Revolution in American Business, Harvard/Belknap, 1977 (Pulitzer Prize, 1978)

- Pulp Fiction, dir. Quentin Tarantino, 1994 (Winston Wolf — Harvey Keitel) · Office Space, dir. Mike Judge, 1999 (Tom Smykowski, the email edition’s shim-in-chief) — cultural anchors, not this week’s news

- Prior CO/AI issues referenced: The Doors of Perception, Jul 7 · The Turk Retires, Jul 6 · Show Me the Money, Jul 1 (email edition) · Git-R-Done, Jun 30 · Central Casting, Jun 23

More like this

The Doors of Perception

Huxley called the mind a reducing valve the lens all work squeezes through. Anthropic just found Claude's, and measured it: 25 concepts wide to our four, and readable for the first time.

The Turk Retires

America turns 250 the same week Bezos's "artificial artificial intelligence" machine files for retirement. The fake automaton always had an expert hidden inside — now the expert steps out of the box and trains the real one. Your filing cabinet is the moat.

Show Me the Money

The benchmark that grades AI like a paying client just went from 2.5% to 16.1% in eight months, and Palantir's CEO is on national TV screaming the pricing question.